Over the last decade, mobile revenues have driven global telecom earnings. But could that change?

Some might argue that fixed networks are poised for a period where investments in that segment have less risk, and faster revenue growth, than the mobile segment.

That might not necessarily mean that fixed networks grow faster than mobile, but that fixed network revenues decline less than mobile revenues, in many markets.

Oddly enough, if mobile revenue growth slows enough, improved fixed network revenue growth would at least change the composition of revenues in the direction of fixed networks.

Though some might disagree, at least some service providers might now believe building and operating gigabit networks represents a revenue growth opportunity, beyond Google Fiber and the handful of municipal or other gigabit networks in operations or trying to get off the ground in the United States.

In some Western European markets, there might also be some new thinking that faster revenue growth is possible in the fixed network high speed access market, than in the mobile segment.

In some ways, those prospects are relative. Recent tier one service provider results in Western Europe show faster decline in mobile retail revenue than in fixed.

Researchers at Analysys Mason argue that, at the very least, fixed network revenue will hold up better than mobile revenue, and also that the share of total revenue generated by fixed networks will grow over the coming five years.

That might require a nuanced assessment, as a change in revenue contribution represents, in large part, a deceleration of mobile revenue.

The unanswered question is the relative value users now place on fixed access and mobile access services. It might be assumed that the value of mobility “always” is higher. But churn rates in the recent recession since 2008 show that at least in some countries, such as Spain, users abandoned mobile services and kept fixed services.

And one key change in the market is the relative value of Internet access and voice services. You might argue that the value of mobile voice is marginally challenged by the growing importance of Internet access as the key value for any access network.

In other words, the single most crucial service is Internet access, and fixed line services in most markets represent a better value proposition than mobile Internet access. And one might argue the value of mobile voice also changes under such conditions.

According to Analysys Mason analysts, mobile revenue in most Western European countries has decoupled from changes in gross domestic product, and is now performing significantly worse than the economy is, as a whole. That, one might suggest, also indicates that, in some instances, mobility has less value to end users than Internet access.

Also, fixed networks also are less dependent on voice revenue than are mobile networks, exposing the mobile segment to greater potential losses.

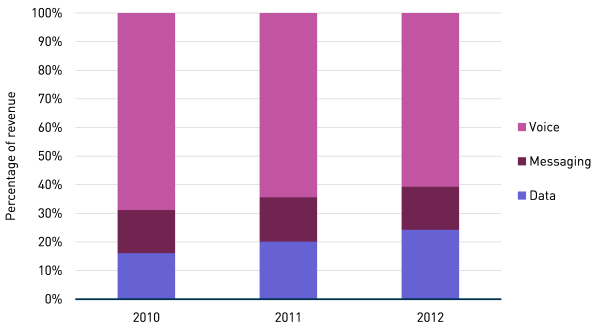

Service revenue from services other than IP data accounted for 76 percent of the total for mobile in 2012 in Western Europe.

Mobile retail revenue by type, Western Europe, 2010–2012 [Source: Analysys Mason]

Fixed operators' exposure to voice is substantially lower. About 67 percent of fixed operator revenue (excluding content) in Western Europe comes from data services in 2012.

Fixed retail revenue by type, Western Europe, 2010–2012 [Source: Analysys Mason)

Also, mobile voice appears to be the most discounted service in quadruple-play packages, leading to “a swift erosion of the value of mobile voice in the market as a whole,” Analysys Mason says.

For example, almost all of the revenue and earnings erosion caused by Free Mobile's entry to the French market was attributed to mobile services, whereas revenue attributable to fixed-line services did not shift from its long-term trajectory.

Fixed service revenue arguably might be less exposed to economic downturns than mobile, as well. Again, it is a bit of a nuance, but fixed network revenue might be more stable than mobile revenue, over the next five years, in many markets.

But there is a wild card. As most mobile devices are equipped for Wi-Fi access, and as those devices become content consumption platforms, with most usage at indoor or at least stationary locations, it is more feasible for Wi-Fi access to provide the Internet access.

And that potentially means fixed-only networks could disrupt much of the “mobile” Internet access value proposition.

0 comments:

Post a Comment