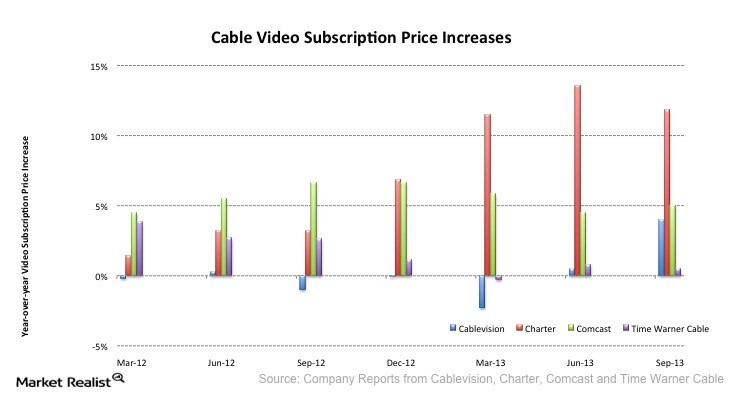

No prediction is required where it comes to expected 2014 price levels for video subscription services. They will rise. They always do.

No prediction is required where it comes to expected 2014 price levels for video subscription services. They will rise. They always do. DirecTV hasn’t announced the precise amount of the increase, but something on the order of a four percent rate increase is logical, after an increase of 4.5 percent or so in 2013.

Comcast typically hikes prices about five percent a year. It is possible the aggregate 2014 rate hikes will amount to about three percent.

Comcast typically hikes prices about five percent a year. It is possible the aggregate 2014 rate hikes will amount to about three percent. In 2013, Dish Network raised prices between seven percent and 20 percent. Another hike, of course, is coming in 2014. Some predict a price increase of about $5 a month, sometime in February 2014.

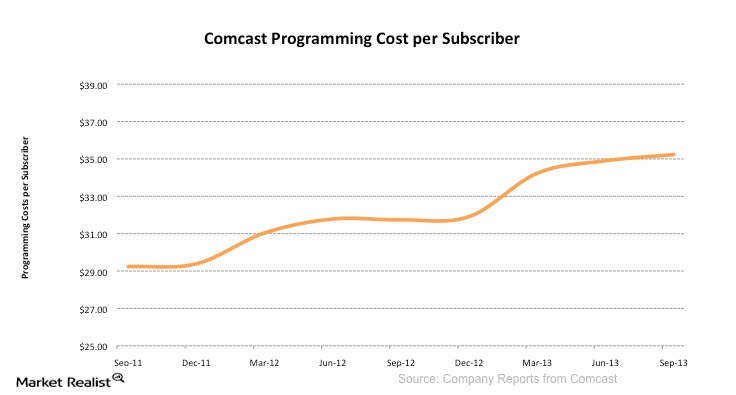

To be fair, those increases largely reflect increases in distributor programming costs. Time Warner Cable’s 2014 payments just to CBS will triple, some predict.

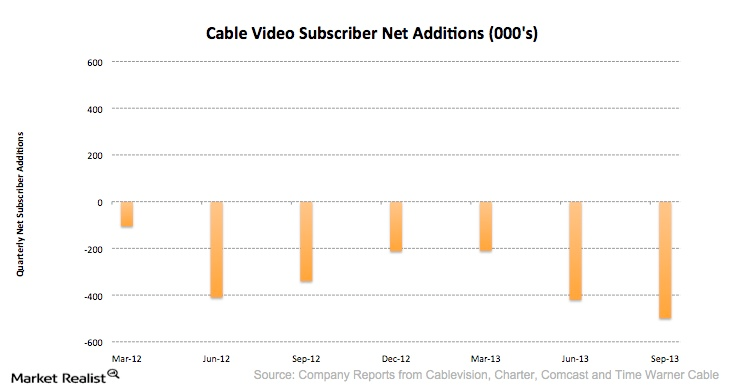

Some argue those annual price hikes, which consumers almost always say they object to, are the reason people slowly are falling out of the habit of paying for traditional video subscriptions.

Some argue those annual price hikes, which consumers almost always say they object to, are the reason people slowly are falling out of the habit of paying for traditional video subscriptions.There is a more dangerous explanation, though. Many younger users find they do not appreciate the product enough to buy it, even when the actual price is really not the barrier.

But higher prices eventually are going to convince greater numbers of people they can do without the subscriptions, and substitute other behaviors, especially as it is easier to display Internet-delivered content on a standard TV.

To be sure, a major change in buying habits likely will not happen until people can buy, at prices they believe are reasonable, much of the content they now expect to view when they buy a video entertainment subscription. That is a ways off, it would seem.

But pressure slowly is building. That doesn't mean an immediate collapse of the current model. But neither would it be unrealistic to predict that, at some point, a major disruption will happen.

But pressure slowly is building. That doesn't mean an immediate collapse of the current model. But neither would it be unrealistic to predict that, at some point, a major disruption will happen.Typically, major changes in consumer behavior happen rather suddenly, when a better alternative to a desired existing product emerges. Globally, there was an inflection point reached sometime early in the 1990s.

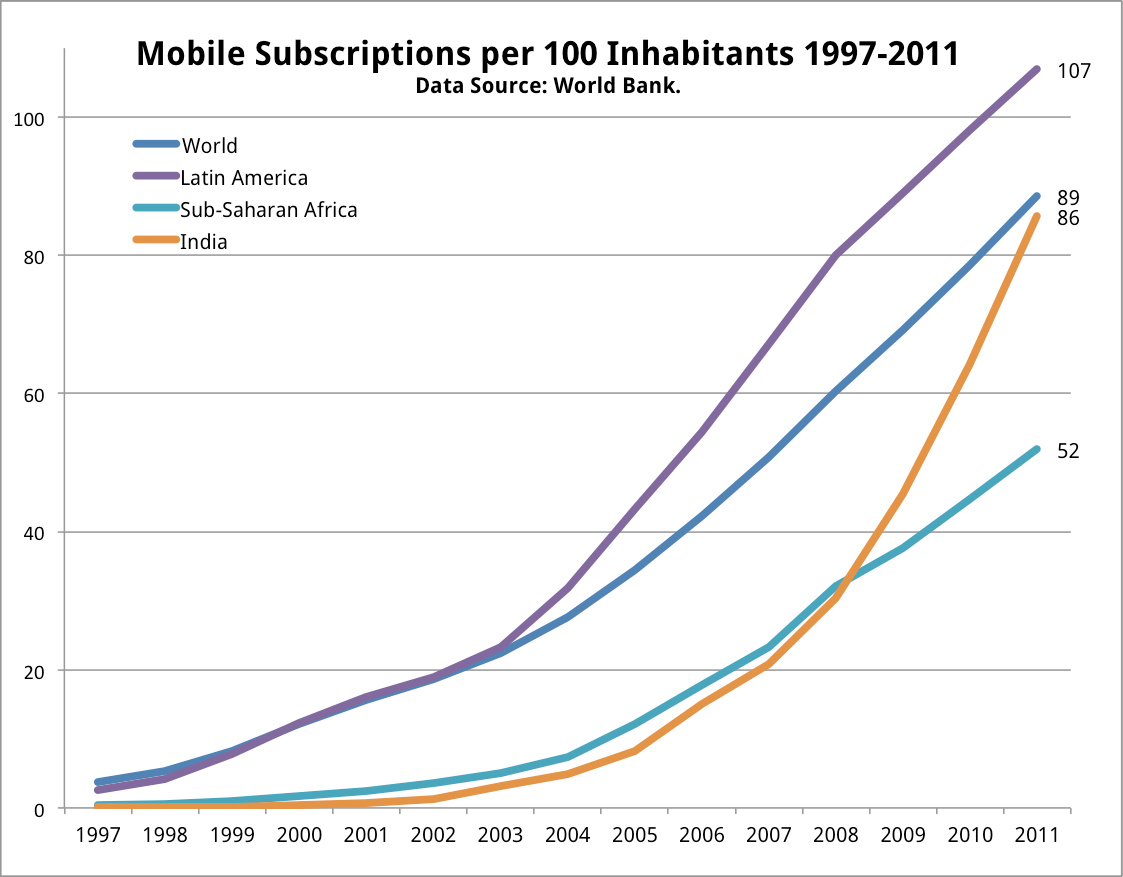

An analogy from the mobile adoption rate in most developing markets provides another example.

An analogy from the mobile adoption rate in most developing markets provides another example.

About 2003, an abrupt change in buying and adoption occurred. The video subscription business can be likened to the long period prior to 2003. The change, in other words, will be discontinuous, not gradual and linear.

0 comments:

Post a Comment