At a high level, all mobile and fixed network service provider strategy is about harvesting legacy revenues at the highest possible rate as new revenue sources are being developed. That has all sorts of implications, ranging from retail packaging of existing products to investments in promising new areas.

And nowhere are the strategic implications more pronounced than in the areas of applications used by smart phones and video entertainment services. As already is clear, smart phones are platforms for consumption of Internet-delivered content, messaging, voice and transactions.

And though observers and some entrepreneurs have envisioned head to head competition between Wi-Fi networks (aided by public or outdoor networks, and anchored by indoor and at-home use) for at least a decade and a half, most would agree that today, Wi-Fi networks are supplemental to, not direct replacements for, access using a mobile network.

When another decade has passed, we might be looking at dramatic structural changes in the “mobile phone” and “video entertainment” businesses, affecting revenue streams for cable TV operators, fixed network telcos and mobile service providers alike.

If past competition between telcos and cable operators has relevance, the issue will be how much core market share each contestant loses, or gains. In the past rounds of competition, telcos have lost voice share while telcos have gained video entertainment share, while splitting Internet access share unevenly (cable has gained more than have the telcos).

But those inter-segment market share wins and losses might also feature something new, namely potential losses between one cable operator and another. For the most part, U.S. cable operators politely refrain from competing with each other.

But technology and revenue pressures seem to be pointing at a future where the industry’s famous collegiality is put to the test. Over the top video is the likely facilitator, in that case.

Everybody seems to agree on the fundamental outlines of the coming revolution. Sooner or later, most of the content people want to pay for will be made available for Internet delivery.

Some ISPs, and especially mobile service providers, may well see a new opportunity to compete for those video entertainment revenues nationwide, irrespective of traditional franchised video service territories.

It also seems likely one or more entities in the cable industry might simply conclude the trend is inevitable, and, at some point, could launch a cable-owned over the top video streaming service.

Mobile service providers, on the other hand, face a place-based challenge, since some 80 percent of smart phone content already seems, in many markets, to be consumed on Wi-Fi networks.

There will remain substantial and clear value for a fully-mobile service, especially for real-time communications. But much content consumption can be handled and consumed when people are stationary. That makes public Wi-Fi a more-compelling alternative, though not a perfect substitute.

Still, those are “tomorrow” issues. Most service providers will do better, financially, to harvest legacy revenues under pressure as best they can, by staving off subscriber account losses and maintaining average revenue per account, on their core products.

No matter how successful, service providers cannot make as much gross revenue or profit from new lines of business as they can by protecting existing core services. The classic example for a fixed network telco is VoIP strategy. Some might argue telcos should have embraced VoIP fully, as the “next generation voice” product.

That has been the strategy for attacking service providers, such as cable operators and hosted IP telephony providers, since they have no legacy customer base to protect. Under such circumstances, those providers were free to package and price as they saw fit.

Telcos were in a different position. If the assumption is that a VoIP service “should cost less,” telco marketers were faced with a choice essentially of “two evils.” They could drop prices across the board to “VoIP” levels, and maintain market share. Or they could simply decide to lose market share, and maintain existing prices and feature sets.

One might argue the wiser course was to trade lower prices per account to maintain market share. It will suffice to note that many service providers, especially in the more-robust North American markets, have chosen to lose some market share rather than adopt across the board price cuts.

But markets differ. In other regions, where there is significant customer defection to VoIP services, some service providers have chosen to offer their own, lower-priced VoIP products.

Neither strategy (across the board price cuts to preserve market share, or maintaining prices while losing share) is right for every service provider in every market.

Now the issue is being addressed in the messaging market, where over the top alternatives are displacing carrier-provided text messaging. Fundamentally, the choices are the same: compete or harvest, where competing almost certainly cannibalizes high-margin text messaging and harvesting means giving up market share.

Some service providers in North America are essentially taking a middle stance, protecting a substantial portion of voice and messaging revenues by making them a feature of access service, while shifting variable consumption-related charges to Internet access service. That’s the basic approach taken by Verizon Wireless and AT&T Wireless, for example.

In other cases, mobile operators can, or must, tap into the over the top opportunity, some would argue.

The issue is that some project OTT revenues will grow from $7.9 billion in 2013 to $53.7 billion in 2017, used by 2.1 billion smart phone users by 2017, a study by mobilesquared suggests.

“Mobile operators should consider such measures as renting mobile numbers or terminating OTT traffic,” argues José Garcia, tyntec VP.

The study suggests Skype is costing the telecom industry $100 million worth of revenue each day, or about $36.5 billion a year.

That likely assumes that Skype’s 280 million active users use two billion minutes each day on Skype calling, and that nearly all those minutes represent lost telco revenues. Many would likely suggest two different processes are at work.

In some cases Skype likely does directly cannibalize usage that otherwise would have been charged on a phone account and therefore created revenue for a service provider.

But it also is the case that much of that activity simply would not have occurred at all, were Skype not available.

Still, fully 43 percent of mobile operators now say that Skype presents a major threat to their revenues.

Of the operators interviewed, 14 percent claimed that OTT services have created a loss of messaging revenue of more than 21 percent in the last year. The same sort of process undoubtedly is at work for messaging services as well.

Of the operators interviewed, 14 percent claimed that OTT services have created a loss of messaging revenue of more than 21 percent in the last year. The same sort of process undoubtedly is at work for messaging services as well. Some traffic likely was shifted from text messaging to over the top alternatives. But much of that over the top activity likely would not have occurred if text messaging were the only alternative.

To be sure, service provider executives do predict that users will rely on OTT messaging services to a greater extent in the future. About 20 percent of service provider executives surveyed estimate that more than 50 percent of their subscribers already use over the top messaging.

WhatsApp has grown by 233 percent in just 12 months and now has 300 million users globally, the study suggests. In that time, WhatsApp daily messages sent have increased from two billion to 10 billion.

The tyntec-sponsored study surveyed more than 40 mobile network operators and mobile virtual network operators in 68 countries as part of the study.

The number of operators reporting no reduction in messaging revenues has sharply deteriorated from 62 percent of service provider operations in 2012 to 36 percent in 2013.

Although some mobile operators have created their own OTT services, this option is largely losing its appeal, the study suggests. IN 2012, about 26 percent of respondents were interested in doing so. In 2013, about 21 percent of mobile operators reported they were interested in doing so.

The percentage of mobile operators interested in partnering with OTT providers grew to 36 percent of respondents, up from 32 percent in 2012.

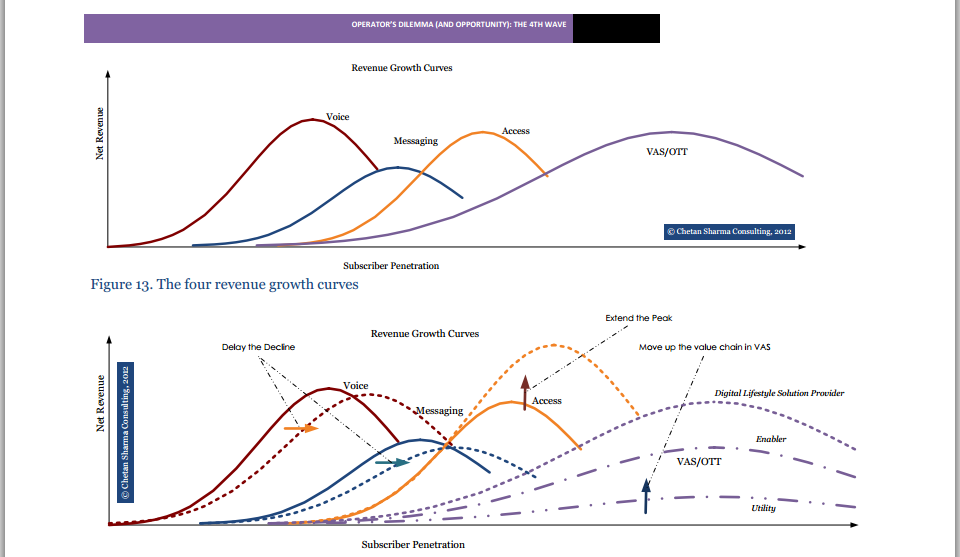

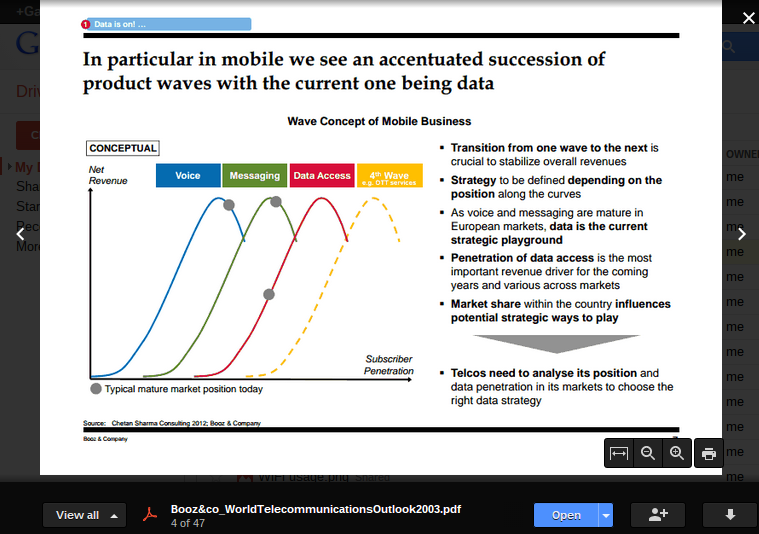

But those efforts to harvest legacy revenues are only part of the challenge. Service providers must also find new replacement revenue sources of some size.

Unlike revenue sources in the first three waves, it is highly likely that the discrete revenue opportunities in a fourth wave, if based on revenue earned largely from over the top app providers partnering in some way with access providers, will be highly fragmented.

Unlike the largely undifferentiated voice, text messaging and mobile Internet access revenue streams, the fourth wave might feature lots of discrete markets, none of them remotely as large as the voice, text messaging or Internet access markets.

That will put new pressure on mobile service providers to control or reduce overhead costs, and create many sophisticated new forms of value to sell to potential business partners. The over-used phrase “agile” comes to mind, but the appellation is not far from the mark. Access providers will have to be much more nimble than in the past to support the many new types of business partners.

The danger, of course, is that other providers could enter the market. Some obvious names typically bandied about include Google, Apple, Amazon, Twitter, Microsoft, Facebook, Visa or PayPal.

0 comments:

Post a Comment