Though it is a nuanced finding, a recent J.D. Power survey of mobile handset satisfaction suggests attributes of the service provider experience (network quality, coverage, customer service, pricing, device availability) influence consumer choice of carriers, even when the same handsets are available from more than one service provider.

The good news is that the service provider “experience” matters. The bad news is that it might not matter as much as some think.

"It's very interesting to see that satisfaction performance differs by smart phone brand across tier one carriers," said Kirk Parsons, senior director of telecommunications services at J.D. Power. "This indicates that carrier services and how these carriers position specific features and services on their devices influence the experience customers have with their smart phone device."

"It's very interesting to see that satisfaction performance differs by smart phone brand across tier one carriers," said Kirk Parsons, senior director of telecommunications services at J.D. Power. "This indicates that carrier services and how these carriers position specific features and services on their devices influence the experience customers have with their smart phone device."Just how important the service provider experience might be is the issue. At least one other analysis suggests handset issues can be crucial. A study sponsored by Oracle found that perhaps 61 percent of consumers would switch service providers to get access to a handset they wanted.

Consumers in France (48 percent), the Netherlands (40 percent), and the U.K. (45 percent) showed similar signs of loyalty toward their handsets, stating that they too would switch operators to use the handset they wanted.

So at least when a service provider has an exclusive (if temporary) for a desirable device, that can in principle outweigh the other service provider attributes (customer service, network quality, recurring service price, other terms and conditions).

In Germany, however, more than 82 percent of surveyed respondents indicated that they would not switch operators just to get a particular handset.

Beyond those findings, there is little dispute that consumer affiliation with products and brands increasingly is titled in the direction of apps and services reached on the Internet, and not with the “access” function itself. That isn’t a new value proposition. People always have valued the ability to talk more than the value of “phone service,” which is a means to an end.

So it is not surprising that mobile service providers have a “love-hate” relationship with smart phones, especially popular devices. On one hand, smart phones drive adoption of Internet access services, and hence represent the underpinning for industry revenue growth. On the other hand, devices potentially shift consumer allegiance and preferences in favor of the appliance, and away from the service provider’s brand.

Still, popular devices that require Internet access are the closest thing to a “personal emotional personification of the service” that mobile service providers or telcos ever have found. Think of the difference between the high emotional involvement people have with products such as perfume, autos, clothing or sports equipment, compared to intangible products such as “dial tone,” “Internet access” or “messaging.”

All other things being equal (wise observers will note that this almost never is completely true), getting customers on service contracts, as much as consumers might not prefer it, could be the single most-important action a mobile service provider can take to reduce customer churn.

To be sure, any number of important issues, ranging from recurring service cost, handset cost, handset selection, customer service, call quality, Internet access speed, billing accuracy and simplicity or network coverage can be a triggering issue for a customer decision to change service providers.

But you might also argue that maintaining significant differences--much less uniqueness--on any of those attributes is virtually impossible to sustain over time. And that might argue for the crucial importance of service contracts as the single most-important element for most service providers (providing postpaid service) in combatting customer churn, ensuring gross revenue and lifetime value of a customer.

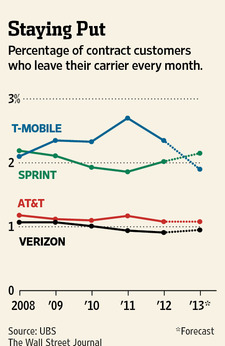

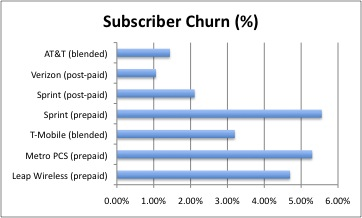

Though the relationship between customer satisfaction and loyalty is highly nuanced, one clear trend of the past several years in the U.S mobile services market is that postpaid or contract customer churn at Verizon and AT&T has been rather low (on the order of one percent a month) while churn has been much higher at Sprint and T-Mobile US (on the order of two percent).

Those are low churn figures for a consumer or business service, where churn sometimes reaches three percent a month.

Prepaid accounts, sold without contracts, have significantly higher churn, at every company. Though mobile customer churn rates generally have declined since 2010, there remains a huge difference between contract customer and no-contract customer churn rates.

Where a prepaid account can last two years or less, a contract-based postpaid account often can last six years to eight years, according to company reports.

And one might therefore be quite tempted to argue that it is the contracts which account for the big differences in churn behavior, even if all other elements of the experience (service and handset prices, perceived value, network quality, customer service, handset selection) are roughly comparable, which tends to be the case.

Prepaid services, for example, are typically synonymous with “no contract” service. Postpaid services more commonly are contract based.

In many markets where prepaid service is the norm, monthly churn rates of four percent are common, leading to annual churn of about 48 percent, of the equivalent of nearly half the entire installed base of customers.

Where churn is one percent a month (characteristic of postpaid services), it takes about four years for a service provider to lose the equivalent of half its customer base.

So any change in the way service is sold (a genuine shift away from contract-based service) should also have churn implications, with direct implications for profit margin, lifetime value of a customer account and gross revenue as well.

In that sense, the growing use of prepaid services in the U.S. mobile market is a strategic problem for most mobile service providers whose financial performance is driven by postpaid and contract service.

The basic issue, where customers can, and do change service providers, is how to reduce the propensity to churn. And though “quality of the network” can be a problem, it might not be the most common reason for a customer to experience an issue leading to choice of another service provider. And price arguably is a disproportionate driver of churn.

The basic issue, where customers can, and do change service providers, is how to reduce the propensity to churn. And though “quality of the network” can be a problem, it might not be the most common reason for a customer to experience an issue leading to choice of another service provider. And price arguably is a disproportionate driver of churn. Though 53 percent of consumers across Europe had been with the same operator for the

past five years, 34 percent of consumers across Europe have been with two operators

in the past five years, and a further 12 percent reported that they have been with three or more

mobile networks in the same time frame.

Among Apple smart phone owners, user satisfaction with their overall experience is highest among Verizon Wireless customers (861), according to J.D. Power. Among Samsung smart phone owners, satisfaction is highest among Sprint customers (853).

Smart phone models that perform particularly well across all four U.S. national carriers include the Apple iPhone 5; Blackberry Z10; Nokia Lumia 920 and Samsung Galaxy Note II, the study found.

The primary reasons for purchasing a smart phone device differ by carrier. Sprint customers are more likely to purchase their smart phone device because of phone features, while T-Mobile customers are more likely to select their smart phone due to price.

The primary reasons for purchasing a smart phone device differ by carrier. Sprint customers are more likely to purchase their smart phone device because of phone features, while T-Mobile customers are more likely to select their smart phone due to price.Still, one might well argue that the single most-significant step service providers can take to reduce customer churn is to get customers on multi-year contracts.

Service provider differentiation in the mind of the buyer seems much clearer in the small business market.

The small business satisfaction survey, conducted among very small business customers (companies with between one and 19 employees, with a corporate service plan) and small and medium business customers (companies with between 20 and 499 employees) does show significant differences between the top-four U.S. providers, especially between Verizon Wireless and AT&T.

The conventional wisdom for most people, including executives at mobile service provider companies, is that there is a relatively direct relationship between "customer satisfaction" and customer churn. In other words, "happy customers" don't leave.

It doesn't appear that is the case. Perhaps perversely, even happy customers will churn (leave a supplier for another), and at surprisingly high rates.

Two out of three (66 percent) wireless and cable TV consumers switched companies in 2011, even as their satisfaction with the services provided by those companies rose, according to Accenture.

The paradox is that “customer satisfaction” does not lead to “loyalty.”

The Accenture Global Consumer Survey asked consumers in 27 countries to evaluate 10 industries on issues ranging from service expectations and purchasing intentions to loyalty, satisfaction and switching.

Among the 10,000 consumers who responded, the proportion of those who switched companies for any reason between 2010 and 2011 rose in eight of the 10 industries included in the survey.

Wireless phone, cable and gas/electric utilities providers each experienced the greatest increase in consumer switching, moving higher by five percentage points.

According to the survey, customer switching also increased by four percent in 2011 in the wireline phone and Internet service sectors.

Sometimes “customer satisfaction scores” have to be evaluated carefully, as it is not clear what predictive value such scores actually have. There are often multiple reasons.

Though customer satisfaction logically is related in some way to customer retention and churn, the relationship is complicated.

Even “satisfied” or “very satisfied” customers will churn, because the other providers are perceived to provide equally-good experiences, and might from time to time also offer better prices or features.

But there are other instances where even rising satisfaction scores are perhaps not what they seen. Consider the example of a declining business, such as fixed network voice services, which might shed about half its subscribers over a decade.

As consumers bleed away from fixed network service providers, satisfaction scores are rising, because the unhappy customers are leaving. Those who remain are more satisfied than the customers who have left, according to the American Customer Satisfaction Index (ACSI).

The fixed-line industry’s ACSI score got better nearly six percentage points, reaching 74, with gains for individual companies ranging from four percent to eight percent, ACSI said. Those are big gains indeed, for the ACSI index.

Verizon improved six percent while Cox gained four percent, to tie for the lead at 74. AT&T follows closely at 73 while Charter scored 72.

CenturyLink’s score improved eight percent, and Comcast got better by six percent, both reaching a score of 71. Time Warner Cable scored 68.

To be sure, it is possible all the fixed network service providers are doing much better than they have in the past. But ACSI also cautions that the reason satisfaction is growing is that unhappy customers are deserting the service.

That might not be such a great way to earn higher customer satisfaction scores.

ISPs were ranked for the first time in the latest ACSI study, and scored the lowest of any industry studied by ACSI.

Internet service providers were rated for the first time, with an average score of 65, the lowest score among all 43 industries tracked by ACSI, which ACSI attributes to high prices, service reliability, speeds and video-streaming quality.

Only Verizon’s FiOS and the aggregate of all other smaller ISPs break out of the 60s with identical ACSI scores of 71.

Cox beats the average at 68, followed by AT&T U-verse and Charter at 65. The low end belongs to CenturyLink at 64, Time Warner Cable at 63 and Comcast at 62.

Video subscription services offered by cable operators, fixed line voice services and even mobile services traditionally have not scored all that high for customer satisfaction, it might also be noted.

Hence the value of service contracts.

0 comments:

Post a Comment