Are global device sales trends a problem or opportunity for Apple, which maintains its “premium device, premium pricing” positioning? It’s hard to tell.

Are global device sales trends a problem or opportunity for Apple, which maintains its “premium device, premium pricing” positioning? It’s hard to tell. Apple can make a reasonable argument that its global positioning will work, as the ranks of consumers able and willing to afford a premium device continues to grow. In other words, gaining a constant share of millions of new “premium segment” consumers across the globe is a big enough market to sustain Apple for the medium term, in its phone business.

Apple assuredly will lose overall device market share over time, but maintain its profit margins, and continue to grow, since the market segment it is targeting is growing. What worries many observers is the analogy to the old PC business. In contrast, Apple arguably took the opposite tack in the MP3 device market, creating products for every price segment.

And, in truth, Apple could change its course over time, gradually adding lower-priced products, as it did in the MP3 market, only when demand at the high end does reach saturation.

And, in truth, Apple could change its course over time, gradually adding lower-priced products, as it did in the MP3 market, only when demand at the high end does reach saturation. You can make your own decision about whether the “premium device, premium price” approach is a winning strategy for most suppliers, but it can, in principle, work for Apple, so long as Apple does not expect to be the volume or market share leader, in devices.

Some would argue the longer term ecosystem implications are a bit more troublesome, as user scale has direct implications for application ecosystem scale and influence. Lack of scale always had some impact in the PC market. Lack of scale never was a problem in the MP3 device business.

To the extent that a robust application and services capability is a key issue in the smart phone business, Apple has not yet encountered problems. Whether that will become an issue later is an arguable point.

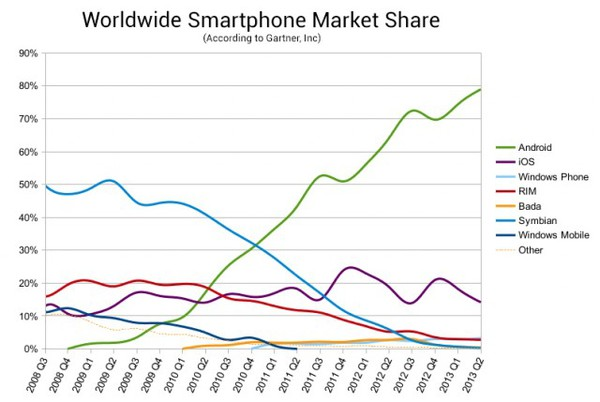

Some might argue Apple’s share will be high enough to sustain a robust application ecosystem, despite the share held by other operating systems and devices. Others will worry. Already, some developers target Android first, Apple second, though hardly anybody thinks Apple is at a strategic disadvantage, at the moment.

Tablet markets might be different. Content for the MP3 player was provided by iTunes and sideloading. Content for smart phones includes both the Internet and the app stores. Content for tablets will be a mix, but similar, in principle, to that of PCs and smart phones.

The issue is the relative roles to be played by Internet accessed content and the app stores. Early on, apps have been crucial for tablet users. Over time, that might change, especially where people use tablets are substitutes for PCs.

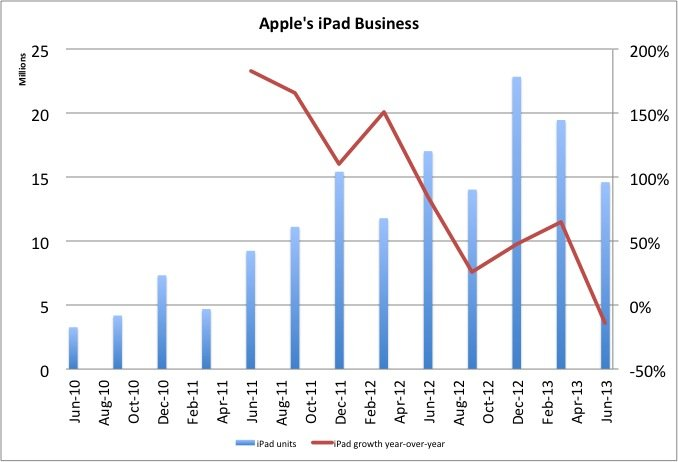

Recent Apple iPad sales have plummeted, in terms of growth rate, for example. There are multiple explanations for that trend, but one might be that people find alternative and more affordable products satisfactory for their desired use cases.

That could be a telling trend. Some consumers might not find affordability to be an issue for any devices, smart phones, tablets or PCs. But most probably will make tradeoffs. People might be willing to spend more for one type of device, less for the others.

One might assume that, when ability to pay is an issue, people will spend on premium devices that are perceived as most personal, less on those devices whose use is less personal.

In other words, propensity to pay a premium in such cases might be highest for the smart phone, less for a tablet and least for a PC.

Global shipments of traditional PCs (desk-based and notebook) are forecast by to total 303 million units in 2013, an 11.2 percent decline from 2012, and the PC market, including ultra-mobile devices, is forecast to decline 8.4 percent in 2013, according to Gartner analysts.

Mobile phone shipments are projected to grow 3.7 percent, with volume of more than 1.8 billion units.

Tablet shipments are expected to grow 53.4 percent in 2013, with shipments reaching 184 million units.

To be sure, some consumers will not have to make any significant tradeoffs, and might well pay premium prices across the board. Most will have to make choices. And the nature of those choices will have key implications for Apple and other suppliers.

0 comments:

Post a Comment