The challenging part of the prediction, though, is that in 2020, revenue levels only will reach 2010 levels.

By 2025, industry revenue will be at about 2009 level, which was higher than 2010 revenue.

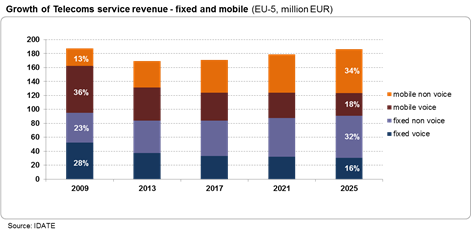

You might call that a “lost decade” of revenue. As you might guess, revenue growth in both fixed network and mobile segments will be driven by non-voice revenues, according to researchers at IDATE.

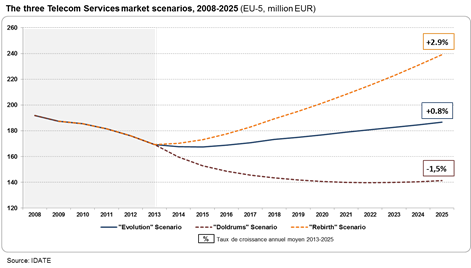

Of course, IDATE researchers also note that performance could be worse, leading to a negative 24 percent revenue performance, or better, in which case revenue could grow 28 percent more than the scenario IDATE considers most likely.

The most likely outcome is based on an assumption that revenue growth for the top five European markets, or EU-5 (France, Germany, Italy, Spain, United Kingdom), will start to grow again in 2016, after shrinking by about four percent in 2013.

In part, IDATE believes the worst case scenario is not the most likely, since it is a simple extrapolation of current trends, with declining voice revenues not matched by growth of new revenue sources.

In part, IDATE believes the worst case scenario is not the most likely, since it is a simple extrapolation of current trends, with declining voice revenues not matched by growth of new revenue sources. The optimistic scenario assumes service providers are successful efforts to generate more money from tiered Internet access (pricing based on consumption) as well as significant new revenue sources. That optimistic scenario has revenue growth of three percent, starting in 2013, something IDATE suggests is not likely.

But even the most likely outcome would require some structural change, one might argue. If you assume new services revenue is likely to be quite modest for the next five or so years, a reversal of revenue patterns would require an ability to charge more largely for existing products.

That would tend to suggest service provider consolidation at a level that significantly reduces the amount of competition, less stringent regulation that allows service providers to raise prices, an ability to tie consumption to pricing, retail packaging policies that raise more revenue per account, growth by acquisition or some elements of each, one might argue.

Up to this point, European service providers have not have notable success boosting prices even for the latest fourth generation Long Term Evolution networks. Mobile data plan retail prices have been dropping, in many countries, since early 2013, according to ABI Research.

ABI Research now has found that Long Term Evolution 4G network tariffs also are falling, either in actual posted prices or as measured by “cost per bit.”

Comparing mobile Internet access pricing between the second quarter of 2012 and fourth quarter of 2012, 73 percent of countries surveyed have reduced the “effective cost” of their 4G tariffs to a significant degree.

The effective cost, measured in terms of “dollar per Gigabyte,” has dropped by 30 percent. In the U.S. market, service providers generally have maintained retail prices, but introduced larger data quotas.

In Australia, Sweden, Japan, and Saudi Arabia the operators lowered the monthly fee but have kept data quotas unchanged.

That state of affairs poses questions, such as whether mobile service providers actually will be able to drive higher revenue, in the near term, from LTE access services.

“ABI Research is concerned that a number of operators have introduced 4G pricing plans at the same, or even lower, price points than 3G,” stated Jake Saunders, VP for forecasting. “In Norway, Telenor has introduced 4G tariffs that are cheaper than 3G.

But one might argue that either the “return to growth” scenario and the “three percent annual growth” scenarios must involve something more than “acquisition by growth.”

Some amount of structural change to reduce the number of suppliers, and retail policies that allow service providers to raise prices (probably requiring regulator policies to change) also seems necessary.

0 comments:

Post a Comment