A problem all public companies have is the tension between managing for long-term growth and quarterly performance, a problem SoftBank CEO Masayoshi Son and Sprint CEO Dan Hesse will continue to face over the next year, and possibly a couple of years.

For starters, Son says it might take that long for Sprint to achieve its objective of the highest customer account gains in the U.S. mobile business. Sprint also will face tough scrutiny from investors who worry about market share growth at the expense of profit margin, and Sprint almost certainly will take that tack.

That is what SoftBank did to take leadership in customer additions in the Japanese mobile market. Assuming Sprint does the same, investors and analysts are certain to loudly voice concern.

In fact, Sprint's compensation policy now ties executive bonuses to subscriber growth rather than revenue growth. Companies tend to produce the results they reward. And Sprint needs to change its organic growth trajectory, as Verizon, AT&T and T-Mobile US are outperforming Sprint.

Like it or not, that is likely what will happen. Sprint will launch aggressive acquisition campaigns, where the value-price relationship will be a key weapon. Average revenue per subscriber or average revenue per account likely will fall. Analysts will object, worry and dismiss Sprint equity.

It is possible SoftBank might try and mitigate some of those problems by working on the value side of the offer, instead of the price.

Since 2007, SoftBank has been Japan's leading seller of smart phones, and many would attribute SoftBank’s success to its offering of more data options for smart phones, tablets, laptops and vehicles, in addition to its pricing attack.

One advantage SoftBank-owned Sprint will not have is an exclusive on the Apple iPhone.

Some would argue Softbank managed to take so much market share in Japan because Softbank had iPhone exclusivity in Japan for the first few years, much like AT&T had in the United States.

The issue is how much SoftBank might be able to do in the area of technology exclusives or distinctiveness.

Some say Sprint’s unlimited smart phone data offers, recently reaffirmed by Sprint, will eventually help.

One might also argue that when Sprint finally does get its Long Term Evolution footprint up to parity with Verizon and AT&T, Sprint might be able to leverage it spectrum holdings from Clearwire to do in the mobile business what Google Fiber has done in the fixed access business, namely reset customer expectations around what an “in line with the market” includes.

In other words, even as Google Fiber is able to sell to a fragment of the U.S. fixed broadband market, it is steadily recasting consumer expectations about speed and price.

Sprint might be planning something similar. And that effort might well hinge on how fast Sprint can build out its whole LTE network nationally.

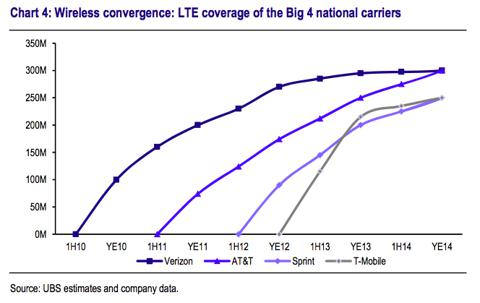

Verizon has nearly completed its LTE deployment, covering nearly 500 markets. AT&T’s LTE coverage is about 400 U.S. markets. Even T-Mobile US, the last national mobile provider to begin building an LTE network, reaches 154 markets.

But it would be reasonable to expect a period of turmoil for Sprint as an equity, not as a business. With a shift of U.S. mobile account growth to prepaid offers, generally with value pricing, both Sprint and T-Mobile US are going to have to work on the value parts of their offers.

One might argue AT&T already is setting up for that struggle by buying Leap Wireless. And that will leave Verizon Wireless will a big challenge. Positioned as the premium provider in the market, Verizon will face a common problem in the communications business: hold its prices and lose share, or drop price to keep share.

Sprint will face an investor relations challenge until it is able to launch its renewed U.S. market assault. Then Sprint likely also will face new criticism about the impact of that attack on profit margins.

Should Sprint succeed, that also means Verizon and AT&T could face more pressure on the investor relations front as well, as they respond. Of course, some might argue there is a possibility Verizon and AT&T will not respond. Some of us would never bet money on that outcome.

0 comments:

Post a Comment